June 2025

Annual Report 2024/25

623 Fort Street

Victoria, B.C.

V8W 1G1

The Honourable Raj Chouhan

Speaker of the Legislative Assembly

Province of British Columbia

Parliament Buildings

Victoria, British Columbia

V8V 1X4

Dear Mr. Speaker:

I have the pleasure of submitting the Office of the Auditor General’s Annual Report 2024/25, as required under section 22 of the Auditor General Act.

Sheila Dodds, CPA, CA, CIA

Acting Auditor General of British Columbia

Victoria, B.C.

June 2025

Accountability statement

This report reflects the performance of the Office of the Auditor General of British Columbia for the 12 months ending March 31, 2025. It was prepared in accordance with the Auditor General Act and the B.C. Reporting Principles. Fiscal assumptions and policy decisions up to June 1, 2025, have been considered in the report’s development.

I am accountable for the results and selection of performance indicators and for ensuring that the information is measured accurately and in a timely manner. Performance data in this report are reliable and verifiable, and any significant limitations in the quality of the data have been identified and explained.

We include estimates and interpretive statements reflecting management’s best judgment. The measures are consistent with our mission, goals, and objectives, and we focus on aspects essential to the understanding of our performance.

Sheila Dodds, CPA, CA, CIA

Acting Auditor General of British Columbia

A message from the auditor general

I’m honoured to present the Office of the Auditor General’s Annual Report 2024/25 and highlights of our work toward the goals, objectives, and performance measures in our service plan. It’s been a year in which we built on the momentum of our achievements and marked the retirement of former auditor general Michael A. Pickup.

Since my appointment as acting auditor general last autumn, I’ve received tremendous support from our teams in financial audit, performance audit, critical audit support, and our executive leadership. I am grateful for their professionalism and each of their contributions to the accomplishments we have shared.

Our annual report demonstrates how we have met our responsibilities under the Auditor General Act. We completed our independent audit of the Province’s Summary Financial Statements, delivered a variety of performance audit reports on government programs and services, and conducted a special examination at the request of the Legislative Assembly.

Internally, I am pleased that we have fully implemented our new compensation policy – a fair, equitable, transparent, and competitive approach to salary progression that reflects work experience and successful job performance.

This report includes the Office of the Auditor General’s annual financial statements, prepared in accordance with generally accepted accounting principles. An independent auditor has audited our financial statements and conducted a reasonable assurance review of our annual report.

I am proud of the achievements summarized here and how they represent our service to the Legislative Assembly and all British Columbians.

Sincerely,

Sheila Dodd, CPA, CA, CIA

Acting Auditor General of British Columbia

Victoria, B.C.

June 2025

Independent Practitioner’s Reasonable Assurance Report

To the Acting Auditor General of British Columbia

We have undertaken a reasonable assurance engagement with respect to the preparation of the accompanying Annual Report (the “Annual Report”) of the Office of the Auditor General of British Columbia (the “Office”) for the year ended March 31, 2025 in accordance with the Performance Reporting Principles For the British Columbia Public Sector (“BC Reporting Principles”). Our observations in relation to this engagement are presented in the attached Appendix.

Management’s Responsibility

Management is responsible for the preparation of the Annual Report in accordance with the BC Reporting Principles.

Management is also responsible for such internal control as management determines necessary to enable the preparation of the Annual Report to conform with the BC Reporting Principles.

Our Responsibility

Our responsibility is to express a reasonable assurance opinion on the Annual Report based on the evidence we have obtained. We conducted our reasonable assurance engagement in accordance with Canadian Standard on Assurance Engagements (CSAE) 3001, Direct Engagements. This standard requires that we plan and perform this engagement to obtain reasonable assurance about whether the Annual Report conforms with the BC Reporting Principles in all significant respects.

Reasonable assurance is a high level of assurance, but is not a guarantee that an engagement conducted in accordance with this standard will always detect a significant deviation when it exists. Deviations can arise from fraud or error and are considered significant if, individually or in the aggregate, they could reasonably be expected to influence the decisions of users of our report. The nature, timing and extent of procedures selected depends on our professional judgment, including an assessment of the risks of material misstatement, whether due to fraud or error, and involves obtaining evidence about the preparation of the Annual Report in accordance with the BC Reporting Principles.

Our Independence and Quality Control

We have complied with the relevant rules of professional conduct / code of ethics applicable to the practice of public accounting and related to assurance engagements, issued by various professional accounting bodies, which are founded on fundamental principles of integrity, objectivity, professional competence and due care, confidentiality and professional behaviour. BDO Canada LLP, a Canadian limited liability partnership, is a member of BDO International Limited, a UK company limited by guarantee, and forms part of the international BDO network of independent member firms.

We apply Canadian Standard on Quality Control 1, Quality Control for Firms that Perform Audits and Reviews of Financial Statements, and Other Assurance Engagements and, accordingly, maintain a comprehensive system of quality control, including documented policies and procedures regarding compliance with ethical requirements, professional standards and applicable legal and regulatory requirements.

Significant Inherent Limitations

As called for by the BC Reporting Principles, the Annual Report contains a number of representations from management concerning the appropriateness of the goals, objectives, and targets established by the Office, explanations of the adequacy of planned and actual performance, and expectations for the future. Management also represents to the extent and nature of information and key performance measures that they believe are critical and meaningful. Such representations are the opinions of management and inherently cannot be subject to independent verification. Therefore, our examination was limited to ensuring the Annual Report contains those representations called for by the BC Reporting Principles and that they are consistent, where applicable with the audited financial statements.

Opinion

In our opinion, the Annual Report of the Office for the fiscal year ended March 31, 2025 conforms in all significant respects with the BC Reporting Principles.

Chartered Professional Accountants

Vancouver, British Columbia

June 20, 2025

Appendix to Independent Practitioner’s Reasonable Assurance Report of BDO Canada LLP on the 2024/25 Annual Report

Observations by the Independent Practitioner

Principle 1 – Explain the Public Purpose Served

The Annual Report explains the Office’s mission and Public purpose, as outlined in enabling legislation. It reports on the organization’s two core business areas and the services/products provided. The Annual Report includes a discussion of the involvement of private sector auditors and the quality assurance measures in place. The Annual Report details the Office’s auditees and stakeholders, including the accountability relationship with the Legislative Assembly. Other factors related to understanding performance are identified, including independence and objectivity.

Principle 2 – Link Goals and Results

The Annual Report identifies the organization’s mission, mandate, goals, objectives, and successfully explains their interrelationships. Performance indicators are reported and reflect the core substance of the objectives and focus on short-term and long-term outcomes. The Annual Report explains the variances between planned and actual results, variances from prior years’ results and discusses plans to achieve targeted results in the future. The Annual Report includes a revised set of measures for future years.

Principle 3 – Focus on the Few, Critical Aspects of Performance

The Annual Report provides information to readers by focusing on key performance indicators that management feels are critical to the understanding of the operational performance of the Office. The results of performance, both financial and nonfinancial, are clearly presented. The Annual Report manages its level of detail by referring appropriately to companion documents.

Principle 4 – Relate Results to Risk and Capacity

The Annual Report examines the key risks to the Office and explains the impact of risk and the resulting critical success factors on performance results. The Annual Report addresses capacity in terms of human resources and information technology infrastructure and how these affect the ability to deliver organizational goals and objectives.

Principle 5 – Link Resources, Strategies and Results

The Annual Report highlights key financial information at an organization-wide level. Explanations are provided for variances from prior year and budgeted amounts. The Annual Report conveys efficiency through its discussions and analyses of performance indicators. Links between resources and outputs are discussed and contribute to the reader’s understanding of the efficiency of operations.

Principle 6 – Provide Comparative Information

Where available the Annual Report provides comparative data in its analyses of the performance indicators.

Principle 7 – Present Credible Information, Fairly Interpreted

The Annual Report covers all key aspects of performance using measures that management feels are relevant. The report clearly identifies the data sources used to assess the performance. The Annual Report is reasonably concise, effectively uses tables and graphs to present information and avoids excessive use of specialized terminology.

Principle 8 – Disclose the Basis for Key Reporting Judgments

The Annual Report identifies the sources of information for performance indicator data. Limitations to data sources, where present, are disclosed. The Annual Report discusses the Office’s confidence in the reliability of the data and reports successes and shortcomings in a fair and balanced manner.

Our mandate

Non-partisan and independent of government, the auditor general reports to the Legislative Assembly of B.C. and provides assurance about government’s financial reporting and program performance. The auditor general is appointed to an eight-year term, as mandated by the Auditor General Act.

The auditor general’s financial audits, performance audits, and other reports provide accurate, objective, and trusted information that supports confidence and improvements in public sector reporting, programs, and services.

The work of the office includes auditing the government’s Summary Financial Statements, which consolidate the financial results of central government and the 138 organizations that make up the government reporting entity (GRE). Organizations in the GRE are controlled by, or accountable to, the provincial government. They include ministries, Crown corporations, universities, colleges, school districts, and health authorities. The auditor general has authority to audit the financial statements of any entity in the GRE and to conduct an audit of the efficiency, economy, and/or effectiveness of any GRE program or service.

We publish a financial audit coverage plan each year that identifies which government organizations’ financial statements will be audited by the auditor general and which organizations will be audited by accounting firms, with oversight by the auditor general.

In addition to prioritizing areas of risk and significance when selecting performance audits, the auditor general considers issues and concerns identified by Members of the Legislative Assembly (MLAs) and the people of B.C. in planning audit work.

The auditor general communicates the work of the office through public reports issued to the Legislative Assembly. Audit reports are referred to the Select Standing Committee on Public Accounts for review and follow up.

Our vision, mission, values, and guiding principles

Our vision

Engaged people making a difference for the people in B.C.

Our mission

We provide independent assurance and trusted information to assist the Legislative Assembly in holding government accountable. Our work contributes to improved financial reporting, programs, and services for the benefit of the people in B.C.

Our values and guiding principles

We believe in supporting each other to learn and develop. Therefore, we will:

- Give people a chance to try new things.

- Delegate responsibilities and support one another in achieving success.

- Be compassionate when things don’t go as planned and coach for success.

We believe in supporting everyone to do their best work. Therefore, we will:

- Recognize everyone’s contribution and celebrate each other’s successes.

- Cultivate an energetic and positive work environment.

We believe in working together as a high performing team. Therefore, we will:

- Collaborate to achieve success.

- Respect people’s position, knowledge, and experience.

- Recognize and value each other’s strengths and interests.

We believe in acting with integrity. Therefore, we will:

- Do what we know is right even when it’s difficult.

- Be kind, straightforward, transparent, and honest in our dealings with others.

- Uphold our high ethical standards.

We believe in being visionary. Therefore, we will:

- Question the status quo and embrace continuous improvement.

- Consult broadly to include diverse perspectives.

- Bravely support new and innovative approaches.

We are committed to creating and reinforcing diversity, inclusion, and safety. Therefore, we will:

- Build a safe environment where everyone feels they belong and is encouraged to bring their whole selves to work.

- Manage our biases and challenge our assumptions around differences.

- Address behavior that discriminates, excludes, or makes someone feel unsafe.

- Make space for all voices.

Our goals, objectives, and key performance indicators

Our goals

- Support each other to do our best work within an inclusive and engaged workplace culture.

- Live our values and work through difficult issues while treating people respectfully.

- Deliver audits and trusted information that demonstrate value from the resources that are entrusted to us.

Our objectives and key performance indicators

Objective 1: Improve clarity and consistency of processes and information used for corporate governance, planning, and reporting

Key performance indicator

- Work Environment Survey – executive-level management driver

Objective 2: Foster an engaged workplace where all employees are safe, supported, and respected

Key performance indicator

- Work Environment Survey – engagement score

Objective 3: Implement a sustainable workforce plan to build organizational capacity and limit operational risk

Key performance indicator

- Employee turnover rate

Objective 4: Maintain and demonstrate the quality of our audits

Due to low response rates with our previous key performance indicator (KPI), we are not reporting a “quality” KPI in 2024/25. As planned, we introduced a more suitable measure of audit quality in our 2025/26 – 2027/28 Service Plan. Going forward, the percentage of staff who meet performance expectations will be our KPI to maintain and demonstrate the quality of our audits.

Objective 5: Deliver our audit commitments on time and on budget

Key performance indicator

- Delivery of independent auditor’s report on government’s Summary Financial Statements

- Delivery of planned number of audit, related assurance, and other1 reports to the Legislative Assembly

1 In past service plans and annual reports, we did not distinguish between assurance reports and other related public reports such as examinations. We have made this change to communicate the purpose and nature of these reports more precisely.

| Goal 1 Support each other to do our best work within an inclusive and engaged workplace culture | Goal 2 Live our values and work through difficult issues while treating people respectfully | Goal 3 Deliver audits and trusted information that demonstrate value from the resources that are entrusted to us | |

|---|---|---|---|

| Objective 1 | Yes | Yes | |

| Objective 2 | Yes | Yes | |

| Objective 3 | Yes | Yes | |

| Objective 4 | Yes | ||

| Objective 5 | Yes |

Our people

Overview

We strive for an engaged workplace where all employees are respected and supported to do their best work within a collaborative environment. This was a transformative year as we launched several initiatives to enhance the culture of our office and demonstrate a strong commitment to employee growth and well-being.

Our 2024/25 Workplace Environment Survey (WES) results highlight the positive impact of the enhancements we have made in our work environment over the past fiscal year. Almost 90 per cent of staff completed the survey. The results showed continued improvement in employee engagement in almost every performance indicator since last year.

Our office experienced some significant leadership changes this year. Sheila Dodds became acting auditor general when Michael Pickup retired. Two senior leaders were promoted to the Executive Committee. We also completed some staff restructuring so that we can focus on our priorities more effectively.

In 2024/25, we completed 16 employment competitions to address operational, technical, and strategic needs. Internal candidates were successful on some of these competitions, supporting the career development of our staff. The external candidates hired through these competitions enhanced our team with new skills and fresh perspectives.

Our new growth-based compensation framework was one of our most significant projects this year. It supports employees as they grow in their careers while providing fair compensation that’s based on experience and performance. The framework introduced performance management processes and systems that support employee growth planning, feedback, and success.

As well, a new progression framework for financial and performance auditors outlines the technical competencies expected for each role – from auditor to director – to support growth within those roles. Behavioural competencies were developed for all staff, helping to contribute to a positive, inclusive, and high-functioning work environment.

Extensive training was provided for employees and managers to create effective goals for their team members, conduct feedback conversations, and complete performance reviews. New procedures help calibrate fair, effective performance-based compensation decisions across portfolios and provide staff with performance recognition. These resulted in significant improvements in role clarity, performance standards, and expectations for development. They also supported considerable enhancements to administrative efficiency and operational effectiveness.

An analysis of the training needs of our staff has also been done to identify training requirements and skills gaps within the office. Other career development initiatives, along with our focus on equity, diversity, and inclusion (EDI), also contributed to employee engagement, retention, and career progression.

This year we saw the full benefits of the leading workplace strategies office renovations that began in the previous fiscal year. Our modernized workplace in downtown Victoria also uses less office space (reduced from three floors to two). The project transformed our work environment and embodies our EDI and accessibility principles (e.g., ergonomic furniture, adjustable lighting, noise sensitive workspaces, wheelchair accommodation, sit/stand desks, gender neutral washrooms, and private wellness spaces). New collaboration spaces offer improved technology for an effective hybrid work environment.

Our IT infrastructure and services underwent extensive updates and improvements this year. We successfully moved to an off-site, professionally managed service environment. The more stable, secure network helps to improve the quality of our work. We also completed a partial review and optimization of business tools that streamlined operations and improved IT support.

Staffing summary (as of March 31, 2025)

Staff at start of 2024/25

133 regular and five auxiliary staff:

- 55% of regular staff had more than one year of experience in their positions

- 45% of regular staff had less than one year of experience in their positions

Staff at end of 2024/25

115 regular and 8 auxiliary staff:

- 82% of regular staff had more than one year of experience in their positions

- 18% of regular staff had less than one year of experience in their positions

Staff breakdown at end of 2024/25

| Critical Audit Support Services | 32 |

| Performance Audit and Related Assurance | 27 |

| Financial Audit and Related Services | 53 |

| Executive, Legal Services and Professional Practices | 11 |

| Total | 123 |

Staffing activities, 2024/25

16 competitions

New hires:

- 10 permanent hires (two from within the B.C. public service and eight from outside)

- Six auxiliary hires

Employee movement:

- Permanent internal promotions: 10

- Auxiliary to permanent status: three

- Internal lateral moves: none

- Internal temporary appointments: eight

- Temporary appointments outgoing to core government: one

- Temporary appointments incoming from core government: one

Departures:

- 18 permanent departures

- Three moved to positions in core government

- Three retirements

Performance indicators

We have many performance indicators designed to support our people and organization.

The Work Environment Survey (WES) is a primary source of indicators. WES is a comprehensive staff survey conducted every two years across the B.C. public service. We choose to conduct this survey annually to gather regular feedback from staff about our organization, culture, practices, and staff engagement.

Objective 1: Improve clarity and consistency of processes and information used for corporate governance, planning, and reporting

Key performance indicator

- Work Environment Survey – executive-level management driver

| 2021/22 Baseline | 2022/23 Actual | 2023/24 Actual | 2024/25 Target2 | 2024/25 Actual | |

|---|---|---|---|---|---|

| Executive-level management score | 59 | 62 | 67 | 66 | 70 |

2 In the 2024/25 service plan, projected targets were 67 for 2025/26 and 68 for 2026/27.

Secondary indicators

- Work Environment Survey – Mission, vision, and values; organization satisfaction; and organization commitment

| 2021/22 | 2022/23 | 2023/24 | 2024/25 | |

|---|---|---|---|---|

| Vision, mission, goals | 72 | 71 | 77 | 77 |

| Organization satisfaction | 65 | 72 | 75 | 76 |

| Organization commitment | 67 | 72 | 74 | 75 |

With a score of 70, we exceeded our 2024/2025 target for executive-level management, attaining our highest score ever.

All secondary indicator results improved from or were consistent with last year. They also reflect the highest scores we have achieved to date.

We are pleased to see these high and improving scores, particularly in a period of transition and change, and will continue to seek ways to build upon them.

Actions taken this year to improve the clarity and consistency of processes and information used for corporate governance, planning, and reporting include:

- a new governance structure to better leverage the strengths of portfolio leaders to support corporate needs and priorities;

- focused touch-base meetings for Executive and Leadership Committees, where priorities and issues are discussed and addressed in a timely and collaborative manner, and effectively shared across portfolios;

- a new strategic plan for 2024 to 2026 to outline our corporate priorities and guide our work;

- a new senior leadership position focused on strategic priorities, performance, and policy;

- new procedures to support effective goal setting and growth planning for all OAG employees;

- processes that enable all staff to directly link their personal goals to the strategic priorities of the office;

- clear role-based expectations and career paths for OAG auditors through financial and performance auditor progression frameworks;

- utilizing the skills of our data analytics and IT teams to support new corporate priorities and reporting needs;

- leveraging IT systems and business intelligence tools for more automated administrative procedures and dynamic, on-demand reporting;

- modernizing our IT infrastructure, supports, and services;

- enhanced communication strategies, including messages from the desk of the acting auditor general;

- piloting corporate governance policies and reporting tools prior to full implementation, and refining based on staff experiences and feedback; and

- obtaining staff feedback through anonymous surveys and staff information sessions.

Objective 2: Foster an engaged workplace where all employees are safe, supported and respected

Key performance indicator

- Work Environment Survey – engagement score

| 2021/22 Baseline | 2022/23 Actual | 2023/24 Actual | 2024/25 Target3 | 2024/25 Actual | |

|---|---|---|---|---|---|

| Engagement score | 66 | 72 | 75 | 72 | 76 |

3 In the 2024/25 service plan, projected targets were 73 for both 2025/26 and 2026/27.

Our 2024/2025 engagement score of 76 surpassed both our target and last year’s results and reflects our highest score yet for this key performance indicator.

Secondary indicators

- Work Environment Survey – Respectful environment, organization satisfaction, teamwork, and empowerment

| 2021/22 | 2022/23 | 2023/24 | 2024/25 | |

|---|---|---|---|---|

| Respectful environment | 76 | 77 | 80 | 78 |

| Organization satisfaction | 65 | 72 | 75 | 76 |

| Teamwork | 82 | 81 | 83 | 86 |

| Empowerment | 69 | 68 | 72 | 72 |

We obtained higher scores in organization satisfaction and teamwork, a consistent score in empowerment, and a lower but still relatively high score in respectful environment.

The overall results are a positive reflection of our efforts to focus on our people and foster an engaged workplace where employees are safe, supported, and respected. Over the past year, these efforts included:

- increased clarity in role and behavioural expectations;

- a clear focus on supporting and recognizing employee growth and success;

- a more modernized physical work environment;

- enhanced technology, networking, and IT supports; and

- a continued focus on accessibility, equity, diversity, and inclusion.

Objective 3: Implement a sustainable workforce plan to build organizational capacity and limit risk

Key performance indicator

- Employee turnover rate

| 2021/22 Baseline | 2022/23 Actual | 2023/24 Actual | 2024/25 Target4 | 2024/25 Actual | |

|---|---|---|---|---|---|

| Turnover rate | 21% | 17% | 13% | 14% | 17% |

4 In the 2024/25 service plan, projected targets were 12 per cent for both 2025/26 and 2026/27.

We also leverage internal human resource statistics to review staffing trends and use those data for a third people-focused key performance indicator on implementing a sustainable workforce plan.

Our 2024/25 turnover rate was 17 per cent for permanent staff, which was above our target of 14 per cent and was four per cent higher than last year. A key factor in this increase was strategic restructuring that resulted in the departure of some staff.

Excluding involuntary exits and retirements, turnover for permanent staff was 10 per cent. We are comfortable with these results and going forward our target is a 12 per cent turnover rate.

Three (17 per cent) of the staff who left our office last year took new positions in core government. As an independent office of the legislature, we are pleased to support employee growth and knowledge and skill transfer across the public service.

We have been a CPA student training office for more than 30 years. Last year we supported six students in their efforts to successfully complete CPA Canada’s Common Final Exam. In 2024, CPA BC conducted a review of our compliance with the CPA pre-approved audit training program and confirmed our ability to train audit-path students. On average, we have 12 students at various stages of the program at any time.

We are also pleased to employ post-secondary co-op students in our office, with three students joining the OAG team in 2025.

Our product

Overview

Our office performs financial audits and performance audits and issues reports on these audits. We also issue reports on other related work, including our annual follow-up report on past performance audit recommendations.

Audits and reports serve the people of British Columbia and their elected representatives by reporting on how well government is managing its responsibilities and resources.

Our audits are conducted in accordance with Canadian auditing and assurance standards.

This year, we issued four performance audit reports, two examination reports, and our annual follow-up report on performance audit recommendations, consisting of 24 separate limited assurance reports. We issued our annual independent auditor’s report on the government’s Summary Financial Statements and 33 independent auditor’s reports for other financial statement audits and assurance engagements.

The quantity and quality of the products we deliver is a credit to the dedication, hard work, and expertise of everyone in our office: from those who work directly on financial and performance audits to the many staff who provide valuable support services that keep our office and audits moving smoothly.

Performance indicators

Objectives 4 and 5 concern our audit work: maintaining and demonstrating the quality of our audits; and delivering audits on time and on budget.

Objective 4: Maintain and demonstrate the quality of our audits

For past service plans and annual reports, we looked to a range of external groups – the Legislative Assembly and the Select Standing Committee on Public Accounts, as well as the public and the government entities we audit – to measure the relevance of our work and how well we deliver it.

As noted in our Service Plan, our former key performance indicator for audit quality relied on an MLA survey but it was not a reliable measure due to low response rates.

After careful consideration, this year we are using the percentage of staff who meet performance expectations as our key performance indicator for maintaining and demonstrating the quality of our audits.

High-performing staff are critical to conducting and delivering high quality audits, and we recognize the important role that all staff play in this regard. The staff performance indicator leverages other strategic priorities and actions in our office, most notably our compensation and growth-based performance management framework and related systems and supports. We will begin to report on this key performance indicator in next year’s annual report.

Public awareness

In 2024/25, we continued to monitor and demonstrate the quality of our audit reports through the indicator of public awareness/perception.

Based on an annual public opinion poll conducted by Angus Reid, we are pleased to see an increase in responses that show positive perceptions of our office. We do note changes in neutral and negative perceptions and will use this information to inform our communication strategies.

| 2021/22 Benchmark | 2022/23 Results | 2023/24 Results | 2024/25 Results | |

|---|---|---|---|---|

| Public perception of our office and our work | Positive: 43% Neutral: 48% | Positive: 43% Neutral: 45% | Positive: 46% Neutral: 44% | Positive:49% Neutral:36% |

| How we measure Positive: Percentage of respondents identifying as “somewhat familiar” or “very familiar” indicating “positive” or “very positive” opinion. Neutral: Percentage of respondents identifying as “somewhat familiar” or “very familiar” indicating “neutral/no opinion.” Source: Angus Reid, March 2025. | ||||

We also recognize some negative public perceptions are to be expected given the mandate of the office, the nature of our work, and the standards we follow. We are careful about how we act on this information.

Additionally, we continue to get positive feedback from the Select Standing Committee on Public Accounts, and from auditees, on their level of confidence in our work.

Objective 5: Deliver our audit commitments on time and on budget

Key performance indicator

- Delivery of independent auditor’s report on the government’s Summary Financial Statements

- Delivery of planned number of audit, related assurance, and other reports to the Legislative Assembly

| 2021/22 Baseline | 2022/23 Actual | 2023/24 Actual | 2024/25 Target5 | 2024/25 Actual | |

|---|---|---|---|---|---|

| Number of audit, related assurance, and other reports tabled with the Legislative Assembly | 12 | 8 | 9 | 9-11 | 7 |

5 In the 2024/25 Service Plan, projected targets were between nine and 11 reports for 2025/26 and 2026/27.

We continue to meet a key audit commitment for our office: the successful delivery of an independent auditor’s report on government’s Summary Financial Statements.

In addition, we produced seven audit, related assurance, and other reports that were tabled with the Legislative Assembly, below our 2024/25 target and 2023/24’s nine reports. A few factors contributed to these results. As noted as a possibility in our Service Plan, the October 2024 general election delayed delivery of some reports. Audit work was also affected as we pivoted to successfully conduct an examination in response to a resolution from the Legislative Assembly, requiring more senior staff time than a typical performance audit. Finally, due to senior staff retirements, leaves, and the need to prioritize attention on complex financial statement audits, reports on government’s audited Summary Financial Statements planned for tabling in March 2025 will be tabled in 2025/26.

Reports by the numbers6

Financial Audit and Related Assurance Work

- one annual independent auditor’s report on government’s Summary Financial Statements

- 18 independent auditor’s reports for financial statement audits

- 15 independent auditor’s reports for other assurance engagements

Performance Audit and Related Assurance Work

- four performance audit reports (two of these audits were published in one public report)7

- two examination reports7

- one annual follow-up report7 consisting of 24 independent review reports of government’s progress towards completing 130 audit recommendations

Additional publications

- Service Plan 2025/26–2027/28

- Annual Report 2023/24

- Financial Audit Coverage Plan

6 For a full list, see Appendix A.

7 Included in the seven audit, related assurance, and other reports reported in our KPI.

Financial audits and related assurance work

Financial statement audits involve an examination of an organization’s financial reporting and accounting and conclude on whether an organization’s financial statements are fairly presented and free of material misstatements (significant errors).

We audit financial statements and provide an independent auditor’s report which provides our conclusion on the accuracy and presentation of the financial statements. The report is at the front of the organization’s financial statements to show whether the statements meet generally accepted accounting principles and that they have been scrutinized by an independent auditor.

We also audit other financial information, such as compliance with federal agreements.

Audit of the province’s summary financial statements

Our office leads the annual audit of the government’s Summary Financial Statements, as required by the Auditor General Act. It’s an important responsibility and a key performance indicator for us.

The audit of the 2023/24 Summary Financial Statements was signed-off on August 15, 2024. Our independent auditor’s report was published with the Summary Financial Statements of the Government of the Province of British Columbia for the 2023-2024 Fiscal Year in the province’s public accounts.

The independent auditor’s report contains two qualifications that highlight that parts of government’s financial statements are not accurate. Qualifications identify errors or omissions the auditor considers so significant that, if uncorrected, might mislead someone who is relying on the accuracy of the information contained in the financial statements.

Our Financial Audit Coverage Plan looks ahead to the next three fiscal years, identifying our level of involvement in the audits of the 138 government organizations, including Crown corporations, universities, colleges, school districts, health authorities, and similar organizations controlled by or accountable to the provincial government. The plan is updated annually, and the current plan was approved by the Select Standing Committee on Public Accounts on March 12, 2025.

Performance audit, related assurance, and other work

Performance audits look at organizations or programs in the government reporting entity to see if they are meeting objectives effectively, economically, and efficiently.

Our work covers a range of different sectors and subjects including:

- Transportation

- Health care

- Education

- Environment

- Justice

- Economic development

- Governance

- Information technology

Performance audit reports provide fair and objective information to MLAs on the performance of programs and services. These reports often include recommendations that have been accepted by government that address deficiencies found through the audit.

In addition to the performance audit and related reports we produced this year, we also support MLAs by following up on past recommendations made by our office. In 2024/25 we published our second annual follow-up report.

Performance audit and examination reports

Examination of MNP’s Administration of the Advanced Research and Commercialization Grant Program (2 reports)

On April 8, 2024, the Legislative Assembly directed, by resolution, the auditor general to “undertake an examination of the administration of grants by MNP LLP under the Advanced Research and Commercialization Program and the Commercial Vehicle Innovation Challenge.” The resolution directed the auditor general to make public an interim report within 90 days and a final report by Sept. 1, 2024.

Our interim report included information on:

- the auditor general’s approach to the examination;

- information about the Advanced Research and Commercialization grant program;

- roles and responsibilities of MNP and the Ministry of Energy, Mines and Low Carbon Innovation in administering the program; and

- examination work completed up to June 2024, and next steps.

Our final examination report was tabled on June 26, 2024, and provided an independent report on the administration of grants by MNP LLP under the Advanced Research and Commercialization Program and the Commercial Vehicle Innovation Challenge.

B.C. Public Sector Boards: Oversight of the Appointment Process

Government oversees the process to appoint members to the boards of about 230 public sector organizations. Each organization has a board to ensure the appropriate use of resources, and that the organization serves the public interest. There are about 2,000 public sector board members who are appointed by government.

Our audit examined whether the Crown Agencies and Board Resourcing Office provided effective oversight of government’s public sector board appointment process to support boards in fulfilling their responsibilities.

Child Care Licensing Capacity (2 audit reports)

ChildCareBC is the provincial plan introduced in 2018 to increase child care access, affordability, and quality. The provincial and federal governments have since funded 39,000 new child care spaces, with about 31,000 more expected by 2028.

We completed two audits focused on the commitment in ChildCareBC to “increase capacity in health authorities to license new spaces, conduct investigations, and monitor compliance.”

Our first audit looked at whether the Ministry of Education and Child Care had worked with health partners to implement the commitment.

Our second audit looked at whether Vancouver Coastal Health assessed if it had the capacity to license new spaces, investigate complaints and monitor child care facilities.

Ministry of Forests: Calculating Carbon Projections

Forest management practices can support climate change mitigation by increasing carbon captured and stored by forests and by reducing forestry emissions. Carbon modelling is used to understand how decisions may change the forest carbon balance.

Our audit examined whether the Ministry of Forests used defined methodologies to calculate consistent and transparent forest carbon projections to inform forest management decisions.

Related assurance reports

Annual Follow-up Report: Performance Audit Recommendations (2019–2022)

Our performance audits of government programs and services often include recommendations for improvement. Organizations respond to these recommendations by outlining whether they accept them and how they’ll implement them.

This was our second annual follow-up report that looked at the progress organizations made in implementing 130 audit recommendations – from 24 audits of ministries, Crown corporations and school districts – published between 2019 and 2022. Preparing this report on an annual basis allows Members of the Legislative Assembly to track the progress organizations make over time.

Performance audits in progress

Our Work in Progress webpage shows performance audits and examinations underway and summarizes their purpose and scope.

Our strategies

We focused on four corporate strategies in 2024/25 to work towards our objectives.

| Objective | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| 1. Continue to improve the quality of our audits | Yes | Yes | Yes | ||

| 2. Create a comprehensive training strategy | Yes | Yes | Yes | Yes | |

| 3. Implement a new compensation framework | Yes | Yes | Yes | ||

| 4. Modernize our IT infrastructure | Yes | Yes | Yes |

Continue to improve the quality of our audits

In 2024/25, we made several improvements that enhanced the quality of our audits. Most notably, we updated our automated financial statement audit methodology to comply with the new group audit standards in the CPA Canada Handbook. Our audit of government’s annual Summary Financial Statements is an example of a large and complex group audit, so these new standards have had a significant impact on how we plan and conduct our audits. As such, this update was a priority for us, as we need to provide our auditors with the tools to support them in this work.

In addition, we automated the forms associated with the initiation and acceptance of an audit or other engagement throughout all our project templates. We have also updated the tools, policies, and procedures we use for initiating and tracking the completion of projects. Under the Canadian Standards on Quality Management, we are required to perform certain procedures prior to committing to carry out any professional activity, like an audit. We take preliminary steps to identify the risks and complexity of the proposed work, and we carry out procedures to ensure we are independent and have sufficient resources to do the work. Our new automated forms provide consistency of process and will automatically flag issues for resolution, which reduces risk and increases our efficiency.

While we have not completed the automation of the performance audit methodology, the automation of the acceptance process was the first step toward this goal. We continue to make progress and plan for further automation of our performance audit methodology, which we will balance with our responsibilities for maintaining our tools in alignment with auditing and assurance standards.

Create a comprehensive training strategy

In April 2024, the terms of reference for our training sub-committee was created. Its four goals will help us maintain an engaged and skilled workforce, through: a competency framework, a needs analysis, learning management system configuration and governance, and roles and responsibilities.

First, we hired a manager of learning and organizational development in August. Next, we created our auditor progression frameworks, which also support our new performance management processes and the analysis of our training needs.

In early 2025, 79 per cent of all staff participated in a comprehensive training needs analysis that identified training requirements and skills gaps. This information will lead to a rolling three-year training and development plan for delivering the right training to the right people at the right time.

Implement a new compensation framework

In 2024/25, considerable achievements were made with respect to developing and implementing a new compensation framework for our office.

In May 2024, we brought in our compensation framework policy to:

- establish a compensation program that is fair, equitable, and competitive;

- support and recognize the contributions and professional growth of our employees;

- promote a healthy performance-based culture;

- support our mandate, strategic goals, and objectives; and

- demonstrate responsible use of public funds.

Last year, we developed many resources, procedures, and systems to support policy implementation, including:

- auditor progression frameworks that outline the technical skills and competencies required at different levels for financial and performance auditors. These will help auditors understand their roles and responsibilities at their current level and at other levels of their careers.

- a behavioural competency framework that outlines desired competencies for all staff with respect to leadership, achieving business results, personal effectiveness, and interpersonal relationships.

- improved performance development and management systems and procedures to support employee goal setting, growth planning, performance discussions, and success.

- a fair and transparent mechanism for staff in management pay bands (MCCF) to determine potential performance-based pay increases after 1827 hours (equivalent to one year of full-time work) in a position. (Salary progression for non-MCCF staff is informed by other agreements or frameworks.)

- data analytic and reporting procedures and tools to effectively and efficiently calculate and report hours in a position since the last performance-based reviews.

- robust procedures and tools to monitor and record decisions, determine potential salary increases, and generate notification letters in a timely and efficient manner.

From December 2024 to March 2025, we piloted and provided staff training on the new resources, procedures, and systems, and made – and will continue to make – refinements based on employee experiences and feedback.

Modernize our IT infrastructure

In the 2022/2023 fiscal year, a comprehensive IT security assessment revealed several critical risks stemming from aging infrastructure and insufficient support for existing systems and applications. In response, the IT Rationalization and Migration Project (RAMP) was launched in January 2024 to address infrastructure vulnerabilities, improve operational resilience, and modernize IT services.

In 2024, the RAMP project successfully moved the in-house data centre to an off-site, professionally managed service environment.

The project also involved a review and optimization of business tools, aiming to streamline operations and improve effectiveness. Software licenses were reviewed and rationalized. New security solutions were deployed. Staff positions were realigned to reflect updated responsibilities and workflows.

Key outcomes included the implementation of a modern intranet site, setting the standard for future development projects while immediately improving content quality for staff. We established business and technical documentation libraries. And we added a new help desk tool to enable the IT team to clarify processes and deliver a consistent service experience for staff.

By January 2025, the full migration of information systems and data was completed, culminating with the formal decommissioning of the old on-site data centre in March 2025. Under budget, the RAMP project delivered substantial cost savings, minimized risk exposure, and introduced significant operational efficiencies. This comprehensive transformation has positioned the organization for improved performance, scalability, and the long-term sustainability of its IT operations while establishing a new level of cybersecurity maturity.

Our finances

Management’s discussion and analysis

In this section, we discuss and analyze our business operations and financial results for the year ending March 31, 2025, as compared to our budget and prior year results. The analysis of our financial performance should be read in conjunction with our audited financial statements and the accompanying notes. Our financial statements have been prepared in accordance with Canadian public sector accounting standards.

Financial and business highlights

The Office of the Auditor General is funded by the Legislative Assembly through a voted appropriation. The vote provides separately for operating expenses and capital purchases. For 2024/25, our budget, based on an estimate of the full cost of operations, was $26.356 million for operating expenses and $263,000 for capital acquisitions.

In 2024/25, the actual cost of our operations was $24.463 million, and our capital expenditures were $255,000. The unused appropriation ($1.89 million for operating expenses and $8,000 for capital acquisitions) cannot be used in subsequent fiscal years. We used 92.8 per cent of our operating budget in 2024/25.

2024/25 financial summary and comparison to plan and prior year

| Expense type | Budget FY25 | FY25 Actual | Variance from budget | FY 24 Actual | Variance Year over Year |

|---|---|---|---|---|---|

| Salaries and benefits | 18,275 | 17,985 | (290) | 16,821 | 1,164 |

| Professional fees | 2,840 | 1,821 | (1,019) | 1,409 | 412 |

| Rental and utilities | 1,700 | 1,668 | (32) | 1,507 | 161 |

| IT expenses | 1,896 | 1,446 | (450) | 881 | 565 |

| Office and other | 583 | 504 | (79) | 856 | (352) |

| Travel | 380 | 376 | (4) | 233 | 143 |

| Vehicle expenses | 17 | 12 | (5) | 16 | (4) |

| Depreciation expense | 665 | 649 | (16) | 228 | 421 |

| Accretion expense | – | 5 | 5 | 3 | 2 |

| Research grants | – | – | – | 70 | (70) |

| Total | 26,356 | 24,466 | (1,890) | 22,024 | 2,442 |

The office remains committed to providing the Legislative Assembly and those we audit with timely, independent, and high-value reports. We issued 34 independent auditor’s reports on financial statements and related information, including our audit report on the province’s Summary Financial Statements. We also issued four performance audit reports, two examination reports, and a follow-up report on past performance audit recommendations. We successfully responded to a resolution by the Legislative Assembly to conduct an examination and report back within months. We realized significant progress on all four strategic priorities, improving the tools and processes supporting the delivery of our audit commitments with an engaged and inclusive workforce. We achieved these results and maintained our workplans with a transition to an acting auditor general.

Operating expenses

Salaries and benefits made up 74 per cent of our total operating expenses. This means that changes or fluctuations in staffing can shift our financial performance significantly from what was planned.

Actual spending on salaries and benefits in 2024/25 was just under $18 million, $290,000 less than planned but $1.2 million more than we spent in the prior year. Our average staffing throughout the fiscal year was 128 full-time equivalents. Turnover this year was 17 per cent for permanent staff, four percentage points higher than the previous year.

Spending on professional service contracts was $1.8 million – $1 million below budget. The underspend was due in part to lower professional services required than expected as we worked to complete significant corporate initiatives that began in the previous year. We have also reduced the proportion of our budget spent on external contractors as we continue to invest in training and retaining our qualified professional staff. In 2025/26 we plan to invest in additional professional staff to build our in-house expertise. Overall, our professional services spending was 36 per cent less than planned.

Audit-related travel continued to increase over the previous few years, indicating a return to pre-pandemic levels. In-person meetings are important to build relationships with those we audit and to enhance our understanding of their organization’s operations and risks. In addition to more travel hours, travel costs have increased because of inflation. These costs came in just under budget but the growth trend means that our travel costs were up about 61 per cent over last year.

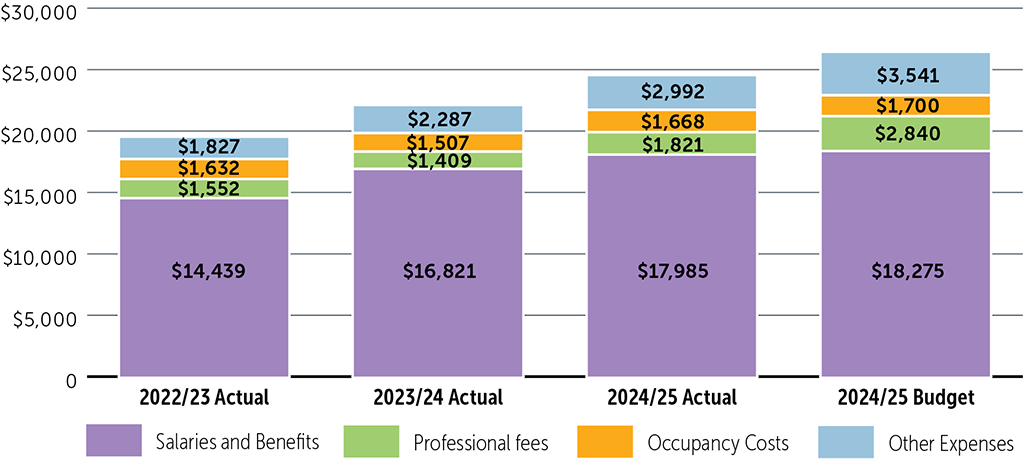

The table below summarizes the changes in key spending categories over the past three years, as well as the 2024/25 budget amounts.

Operating expenses, actual versus planned ($000s)

Operating expenses – tabular data

| Operating expenses | 2022/23 Actual | 2023/24 Actual | 2024/25 Actual | 2024/25 Budget |

|---|---|---|---|---|

| Salaries and benefits | 14,439 | 16,821 | 17,985 | 18,275 |

| Professional services | 1,552 | 1,409 | 1,821 | 2,840 |

| Occupancy costs | 1,632 | 1,507 | 1,668 | 1,700 |

| Other expenses | 1,827 | 2,287 | 2,992 | 3,541 |

Capital purchases

Capital expenditures this year were $255,000, down significantly from the year before, as most of our investments in IT infrastructure and a flexible office work environment were completed in 2023/24.

This year, we invested just over $180,000 to complete our new Data Centre setup, approximately $70,000 to refresh staff IT equipment such as laptops and other peripherals and close to $5,000 to purchase some final pieces of furniture to complete spaces that were renovated last year.

Looking ahead

Looking ahead, we will continue to build on our successes and improvement efforts.

Strategies will include an enhanced focus on the quality and efficiency of our audits and related support functions and increasing capacity to examine areas of growing importance to MLAs and to people in B.C.

Building on considerable work to date, we will fully implement growth-based employee performance development and management processes that align with the strategic needs of the office. To further support employee growth and success, we will also continue to prioritize and implement elements of our employee training and development framework.

Our fiscal 2025/26 operating budget is consistent with the three-year plan approved by the Finance and Government Services Select Standing Committee in October 2023.

Financial statements 2024/25

Statement of management responsibility

The accompanying financial statements of the Office of the Auditor General (the office) are the responsibility of management.

The financial statements have been prepared by management in accordance with Canadian public sector accounting standards. Financial statements are not precise, since they include certain amounts based on estimates and judgments. When alternative accounting methods exist, management has chosen those it considers most appropriate in the circumstances to ensure that the financial statements are presented fairly in all material respects.

We have developed and maintain systems of internal control that give reasonable assurance that the office has:

- operated within its authorized limits,

- safeguarded assets, and

- kept complete and accurate financial records.

The Select Standing Committee on Finance and Government Services of the Legislative Assembly appointed BDO Canada LLP, Chartered Professional Accountants to audit the accounts of the office for the year ended March 31, 2025.

Sheila Dodds, CPA, CA CIA

Acting Auditor General

Nathaniel Morbey, CPA, CA

Chief Financial Officer

External auditor’s opinion on the financial statements

Independent Auditor’s Report

To the Acting Auditor General of British Columbia

Opinion

We have audited the accompanying financial statements of the Office of the Auditor General (the “Office”), which comprise the Statement of Financial Position as at March 31, 2025 and the Statements of Operations, Changes in Net Debt and Cash Flows for the year then ended, and notes to the financial statements, including a summary of significant accounting policies.

In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of the Office as at March 31, 2025 and the results of its operations, changes in net debt, and cash flows for the year then ended in accordance with Canadian public sector accounting standards.

Basis for Opinion

We conducted our audit in accordance with Canadian generally accepted auditing standards. Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We are independent of the Office in accordance with the ethical requirements that are relevant to our audit of the financial statements in Canada, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Other Information

Management is responsible for the other information. The other information comprises the information included in the Annual Report but does not include the financial statements and our auditor’s report thereon.

Our opinion on the financial statements does not cover the other information and we do not express any form of assurance conclusion thereon.

In connection with our audit of the financial statements, our responsibility is to read the other information identified above and, in doing so, consider whether the other information is materially inconsistent with the financial statements or our knowledge obtained in the audit, or otherwise appears to be materially misstated.

Responsibilities of Management and Those Charged with Governance for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with Canadian public sector accounting standards, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, management is responsible for assessing the Office’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Office or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Office’s financial reporting process.

Auditor’s Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with Canadian generally accepted auditing standards will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with Canadian generally accepted auditing standards, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

- Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

- Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Office’s internal control.

- Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management.

- Conclude on the appropriateness of management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Office’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause the Entity to cease to continue as a going concern.

- Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

Chartered Professional Accountants

Vancouver, British Columbia

June 20, 2025

Statement of financial position

| As at March 31, 2025 (in $000s) | Note | 2025 | 2024 |

|---|---|---|---|

| Financial assets | |||

| Petty cash | 2 | 2 | |

| Due from the consolidated revenue fund | 3 | 1,109 | 2,106 |

| Total financial assets | 1,111 | 2,108 | |

| Liabilities | |||

| Accounts payable and accrued liabilities | 1,509 | 2,566 | |

| Asset retirement obligation | 4 | 143 | 138 |

| Total liabilities | 1,652 | 2,704 | |

| Net debt | (541) | (596) | |

| Non-financial assets | |||

| Tangible capital assets | 5 | 3,224 | 3,618 |

| Prepaid expenses | 6 | 398 | 458 |

| Total non-financial assets | 3,622 | 4,076 | |

| Accumulated surplus | 7 | 3,081 | 3,480 |

Approved by:

Sheila Dodds, CPA, CA CIA

Acting Auditor General

Nathaniel Morbey, CPA, CA

Chief Financial Officer

The accompanying notes are an integral part of these financial statements.

Statement of operations

| For the fiscal year ended March 31, 2025 (in $000s) | Note | 2025 Budget | 2025 Actual | 2024 Actual |

|---|---|---|---|---|

| Expenses | ||||

| Salaries and benefits | 18,275 | 17,985 | 16,821 | |

| Professional fees | 2,840 | 1,821 | 1,409 | |

| Occupancy costs | 1,700 | 1,668 | 1,507 | |

| Information technology | 1,896 | 1,446 | 881 | |

| Office | 570 | 488 | 836 | |

| Travel | 380 | 376 | 233 | |

| Depreciation | 665 | 649 | 228 | |

| Accretion | – | 5 | 3 | |

| Research grants | – | – | 70 | |

| Vehicle | 17 | 12 | 16 | |

| Other | 8 | 7 | 7 | |

| Advertising | 5 | 9 | 13 | |

| Total cost of operations | 26,356 | 24,466 | 22,024 | |

| Funding appropriations | ||||

| Operating | 8 | 25,691 | 23,812 | 21,793 |

| Capital | 8 | 263 | 255 | 3,118 |

| Annual surplus (deficit) | (402) | (399) | 2,887 | |

| Accumulated surplus beginning of year | 7 | 3,480 | 3,480 | 593 |

| Accumulated surplus end of year | 3,078 | 3,081 | 3,480 | |

The accompanying notes are an integral part of these financial statements.

Statement of changes in net debt

| For the fiscal year ended March 31, 2025 (in $000s) | Note | 2025 Budget | 2025 Actual | 2024 Actual |

|---|---|---|---|---|

| Net debt at beginning of year | (596) | (596) | (543) | |

| Annual surplus (deficit) | (402) | (399) | 2,887 | |

| Changes in tangible capital assets | ||||

| Acquisition of tangible capital assets | (263) | (255) | (3,118) | |

| Amortization of tangible capital assets | 665 | 649 | 231 | |

| Asset retirement obligation change of estimate | – | – | (67) | |

| 402 | 394 | (2,954) | ||

| Changes in working capital assets | ||||

| Acquisition of prepaid expenses | – | (398) | (458) | |

| Use of prepaid expenses | – | 458 | 472 | |

| – | 60 | 14 | ||

| Decrease (increase) in net debt | – | 55 | (53) | |

| Net debt at end of year | (596) | (541) | (596) | |

The accompanying notes are an integral part of these financial statements.

Statement of cash flows

| For the fiscal year ended March 31, 2024 (in $000s) | Note | 2025 | 2024 |

|---|---|---|---|

| Due from Consolidated Revenue Fund, beginning of year | 3 | 2,106 | 696 |

| Operating transactions | |||

| Cash used to: | |||

| Pay employees or benefits plans | (17,679) | (16,975) | |

| Pay suppliers | (7,130) | (3,408) | |

| (24,809) | (20,383) | ||

| Cash received from: | |||

| Operation appropriation | 23,812 | 21,793 | |

| Capital transactions | |||

| Cash used to: | |||

| Acquire tangible capital assets | 5 | (255) | (3,118) |

| Financing transactions | |||

| Cash received from: | |||

| Capital appropriation | 255 | 3,118 | |

| Increase in due from consolidated revenue fund | (997) | 1,410 | |

| Due from Consolidated Revenue Fund, end of year | 3 | 1,109 | 2,106 |

The accompanying notes are an integral part of these financial statements.

Notes to our financial statements

Year ended March 31, 2025 (tabular amounts in $000s)

1. Nature of operations

The Auditor General is an Officer of the Legislature of British Columbia appointed under the Auditor General Act (the act). The act, as amended March 13, 2013, allows for the appointment of an auditor general for a single, eight-year term by the Legislative Assembly. Non-partisan, objective and independent of the government of the day, the auditor general reports impartial assessments of government accountability and performance to the assembly.

The auditor general’s mandate is established by the act. The act requires the auditor general to audit the government’s annual Summary Financial Statements and allows the auditor general to be appointed as the financial statement auditor of any government organization or trust fund. The act also allows the auditor general to carry out examinations focusing, among other things, on whether government or a government organization is operating economically, efficiently, and effectively; and whether the accountability information provided to the Legislative Assembly by the government or a government organization with respect to the results of its programs is adequate.

Funding for the Office of the Auditor General comes from a voted appropriation (the vote) of the Legislative Assembly.

2. Significant accounting policies

These financial statements have been prepared in accordance with Canadian public sector accounting standards (PSAS).

a. Voted appropriation

The office receives approval from the Legislative Assembly to spend funds through an appropriation vote. The vote provides for both operating expenses and capital acquisitions. Non-cash transactions, such as amortization, are covered by the vote but not recognized as revenue from the appropriation of funds. An annual excess or deficiency of revenues over expenses arises from the difference between revenue recognition of capital appropriations and expense recognized for the amortization of tangible capital assets.

Any unused vote amounts cannot be carried forward for use in subsequent years.

b. Financial instruments

It is management’s opinion that the office is not exposed to significant interest, currency or credit risk arising from its financial instruments.

A statement of remeasurement gains and losses has not been prepared as there are no such gains or losses.

c. Asset retirement obligation

Asset retirement obligations are legal obligations associated with the retirement of tangible capital assets. This includes post-retirement operation, maintenance, and monitoring that are an integral part of the retirement.

Liabilities for asset retirement obligations are recorded when there is a legal obligation to incur retirement costs in relation to a tangible capital asset, the past transaction or event giving rise to the liability has occurred, and a reasonable estimate of the amount can be made.

The costs of asset retirement obligations are recognized over the estimated useful lives of the underlying tangible capital assets.

d. Tangible capital assets

Tangible capital assets are recorded at historical cost less accumulated amortization. Amortization begins when the assets are put into use and is recorded using the straight- line method over the estimated useful lives of the assets as follows:

| Computer hardware and software | 3 years |

| System hardware and software | 5 years |

| Furniture and equipment | 5 years |

| Tenant improvements | Term of lease (ends October 2034) |

e. Presentation of expenses

The office provides audit services for the Legislative Assembly. Audit services include both financial statement audits and performance audits. Since audit services are the office’s sole service line, expenses are presented by object in the statement of operations.

f. Employee future benefits

i. Pension benefits

All eligible employees participate in a multi-employer, defined benefit pension plan. Defined contribution plan accounting has been applied to the plan as the office has insufficient information to apply defined benefit plan accounting. Accordingly, the office’s contributions are expensed in the year in which the employees’ services are rendered and are included as a component of salaries and benefits on the statement of operations. These contributions represent the office’s total obligation for pension benefits.

ii. Other future benefits

Eligible employees are entitled to post-employment health care and other benefits as provided under terms of employment agreements. The cost of these benefits is recorded as employees render the services necessary to earn them. The liability for the other future benefits is managed and recorded by the BC Public Service Agency.

iii. Leave liability

Eligible employees are entitled to accumulate earned, unused vacation, and other eligible leave entitlements as provided under terms of employment or collective agreements. The liability for the leave is managed and recorded by the BC Public Service Agency and not presented in these financial statements.

g. Measurement uncertainty

These financial statements are prepared in accordance with PSAS, which require management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the reporting period. Estimates are used to determine asset retirement obligations. The estimated useful lives of tangible capital assets are the most significant item for which estimates are used. Actual results could differ from those estimates. These estimates are reviewed annually, and as adjustments become necessary, they are recognized in the financial statements in the period in which they become known.

3. Due from the Consolidated Revenue Fund

The office does not have its own bank account or hold cash or cash equivalents. All monetary transactions of the office are processed through the Consolidated Revenue Fund (CRF) of the Province of British Columbia. This balance is reflective of differences in the timing of events that obligate the office, and therefore the CRF, to distribute funds, and the receipt of the benefit from disbursing those funds. The statement of cash flows presents the continuity of this balance and all component flows.

4. Asset retirement obligation

The office has installed tenant improvements in the building that it leases and may be required, by the landlord, to remove them when the lease ends. A liability for the estimated cost of removal has been accrued. The estimated cost to remove tenant improvements when the lease ends in October 2034 is $206,725. Using a discount rate of 3.75%, this liability is recorded as $143,058 at March 31, 2025.

5. Tangible capital assets

| Computer hardware and software | Network hardware and software | Furniture and equipment | Tenant improvements | Total | |

|---|---|---|---|---|---|

| Year ended March 31, 2024 | |||||

| Opening net book value | 246 | 75 | 14 | 329 | 664 |

| Additions | 47 | 1,181 | 461 | 1,493 | 3,182 |

| Disposals | – | – | – | – | – |

| Amortization | (152) | (49) | (5) | (22) | (228) |

| Closing net book value | 141 | 1,207 | 470 | 1,800 | 3,618 |

| At March 31, 2024 | |||||

| Cost | 1,408 | 2,091 | 1,077 | 2,004 | 6,580 |

| Accumulated amortization | (1,267) | (884) | (607) | (204) | (2,962) |

| Net book value | 141 | 1,207 | 470 | 1,800 | 3,618 |

| Year ended March 31, 2025 | |||||

| Opening net book value | 141 | 1,207 | 470 | 1,800 | 3,618 |

| Additions | 129 | 116 | 10 | – | 255 |

| Disposals | – | – | – | – | – |

| Amortization | (109) | (263) | (98) | (179) | (649) |

| Closing net book value | 161 | 1,060 | 382 | 1,621 | 3,224 |

| At March 31, 2025 | |||||

| Cost | 1,537 | 2,207 | 1,087 | 2,004 | 6,835 |

| Accumulated amortization | (1,376) | (1,147) | (705) | (383) | (3,611) |

| Net book value | 161 | 1,060 | 382 | 1,621 | 3,224 |

6. Prepaid expenses

| March 31, 2025 | March 31, 2024 | |

|---|---|---|

| Software and hardware maintenance | 195 | 313 |

| Rents | 145 | 102 |

| Other | 58 | 43 |

| 398 | 458 |

7. Accumulated surplus

The accumulated surplus balance represents the portion of the net book value of tangible capital assets that have been funded through appropriations.

8. Funding appropriations

The office receives approval from the Legislative Assembly to spend funds through an appropriation that includes two components—operating and capital. Any unused appropriations lapse at the fiscal year-end.

The budget for expenses shown on the statement of operations includes depreciation of tangible capital assets and is based on the budgeted expenses approved by the Select Standing Committee on Finance and Government Services.

The following table reconciles the operating appropriation and provides a comparison of current and prior year voted capital and operating appropriations. There are no reconciling items for the capital appropriation.

| Year ended March 31 | 2025 | 2024 |

|---|---|---|

| Voted appropriation, operating | 26,356 | 23,415 |

| Cost of operations | 24,466 | 22,023 |

| Depreciation | (649) | (228) |

| Accretion | (5) | (3) |

| Operating appropriation | 23,812 | 21,793 |

| Unused operating appropriation | 2,544 | 1,622 |

| Voted appropriation, capital | 263 | 3,200 |

| Capital purchases | 255 | 3,118 |

| Unused capital appropriation | 8 | 82 |

9. Employee future benefits